The critical supply chain for fertilizer in combination with rising energy and transport costs will be felt most by poorer countries and households. Whether this develops into a veritable food crisis will depend on how the war procedes.

The Iran war has disrupted critical supply chains and driven up the cost of energy and fertilizer, both essential agricultural inputs, sparking fears of another global food crisis. With input costs soaring, fertilizer exports from the Gulf countries suspended, and production facilities facing unprecedented challenges, the world’s ability to maintain stable food supplies is increasingly at risk.

The input crisis

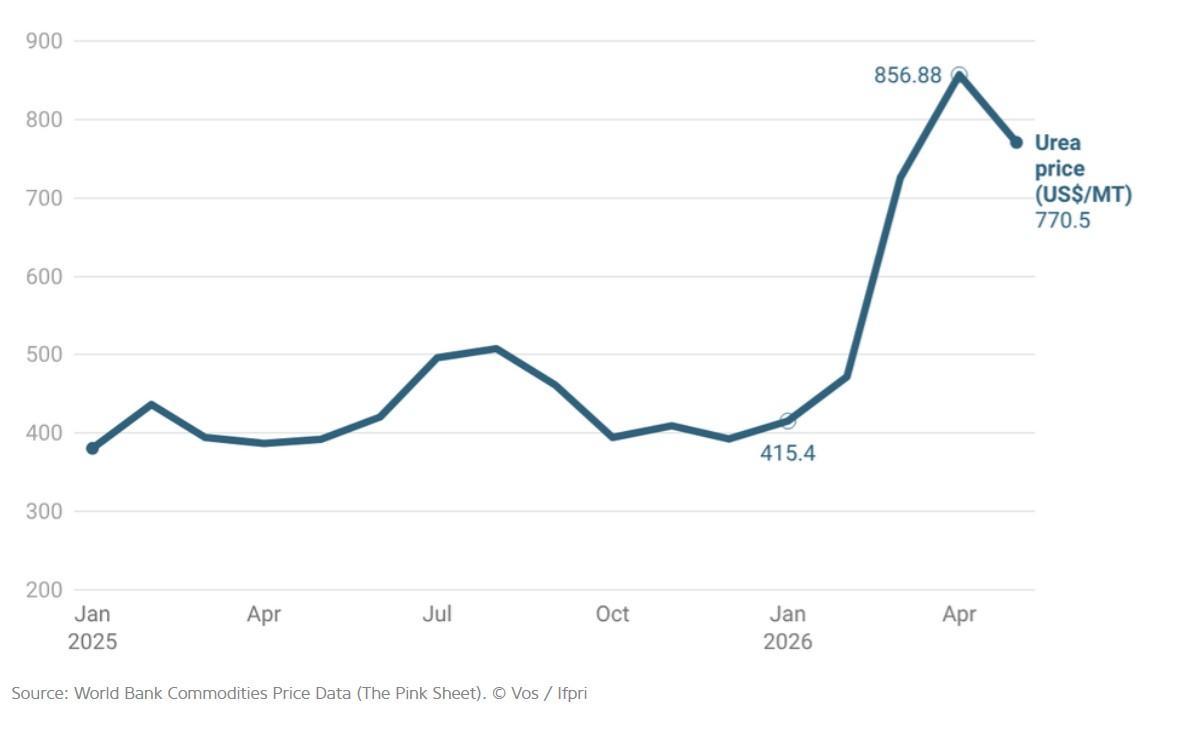

Before the Iran war, fertilizer prices firmed in early 2026, following seasonal demand for spring applications by farms in the northern hemisphere. Prices spiked, however, following the effective closure of the Strait of Hormuz at the end of February 2026, with prices of urea – a key chemical fertilizer – roughly doubling in a matter of weeks (Figure 1). Prices of phosphate (another main type of fertilizer) also increased, though more moderately from already elevated levels. Urea prices softened somewhat during May 2026, as also shown in Figure 1, following China’s announcement to lift its ban on urea exports and weakening of demand as the northern spring application ended (AMIS 2026a). Yet, upward pressure on prices remains high as fertilizer supplies are constrained by the continued closure of the Strait of Hormuz.

The Middle East supplies about one-third of global urea exports. Since the end of February 2026, an estimated 3.9 million tonnes of these exports have been suspended. This is equivalent to 30 percent of annual fertilizer exports of the Gulf States. Most production facilities in the region continue to operate at reduced rates to prevent excessive stockpiling. While urea can generally be stored for several months, high temperatures and moisture can damage its quality. The risk of substantial fertilizer supply shortages is rising as the conflict prolongs and the Strait of Hormuz stays closed.

Figure 1 Surging fertilizer prices (urea price in US$ per MT)

The crisis has also pushed up the costs of manufacturing urea, as prices of key inputs to produce urea (natural gas and ammonia) increased sharply. For phosphate producers, sulphur has become a major cost concern, with prices well above historical averages since 40–45 percent of global sulphur exports usually come from the affected region. Export restrictions from other suppliers have further intensified these price increases. Phosphate markets are even tighter. About 20 percent of the world’s phosphate supply comes from Saudi Arabia.

Continued military strikes into June 2026 and temporary production shutdowns in Bahrain, Iran, and Qatar highlight growing vulnerabilities in this supply chain for agricultural inputs. Restarting a fertilizer plant after a shutdown usually takes five to eight weeks, with structural damage and repairs it can take several years. Meanwhile, other suppliers have partially replaced exports coming from the Gulf region, though at higher prices.

No grain shortage - but increased production costs

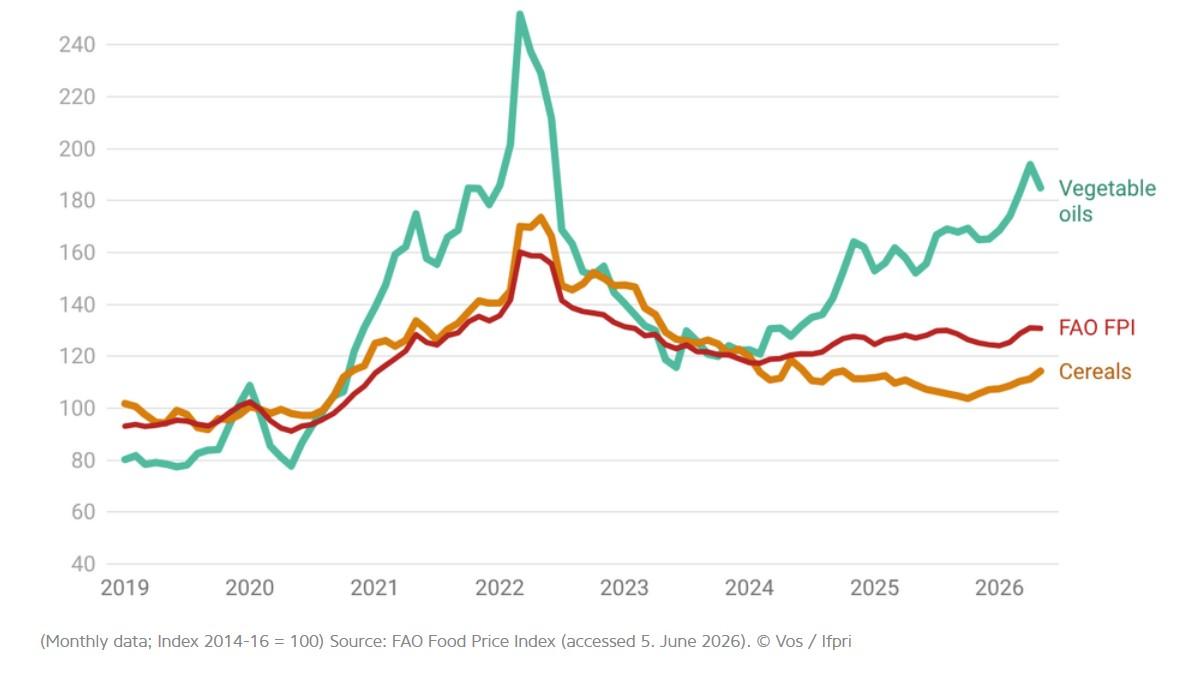

The current situation is different from the global food price crisis that emerged after COVID in 2020 and the beginning of the Russia-Ukraine war in February 2022 (Vos, 2025). That crisis was marked by both grain and fertilizer shortages. The Middle East countries are not major global grain exporters, so there is no direct grain shortage, and international food prices have remained relatively stable, especially for cereals (FAO Food Price Index, Figure 2). Prices of vegetable oils, though, surged since the closure of the Strait of Hormuz, driven in good part by higher prices for oil and demand for biofuels.

Figure 2 International food prices (FAO Food Price Index), since 2019

For now, the warning signs of trouble ahead include rising costs for fertilizer, fuel, shipping, energy for irrigation and other farm equipment, and financing. Higher input prices are already making it more difficult and expensive to distribute and process food. When energy prices increase, transportation and food processing costs go up and it is more expensive to keep food fresh, with a high risk of food losses. The delivery of food assistance will require more financial resources.

Consequently, farmers may decide to use less fertilizer, which would lower yields and food supplies. In the short run, however, the implications of high prices and restricted supply of fertilizer will vary widely depending on reliance on the Gulf region and the extent to which farmers expect farm profitability will be affected by higher input costs.

The effects of the Iran crisis in detail

First, while global fertilizer price increases are being felt broadly, the risk of direct physical shortages differs across major production areas. In the United States, supplies for most farmers were sufficient for spring plantings, but autumn applications of fertilizer could be at risk, depending on how the crisis evolves. Farmers in Brazil are almost fully reliant on imports (of which 40% come via the Strait of Hormuz) and have seen local fertilizer prices jump over 35% in the first two weeks from the start of the conflict. India has enough supply for the kharif crops (sown at the start of the monsoon season in June-July), but rabi (winter) season availability is uncertain due to high dependence on Middle Eastern suppliers of fertilizers and natural gas. Farmers in Sub-Saharan Africa, but especially those in East Africa, are highly vulnerable, as one third of their fertilizer supplies come from the Gulf area. They also face high transport and distribution costs (Vos at al. 2025; Hebebrand et al. 2026).

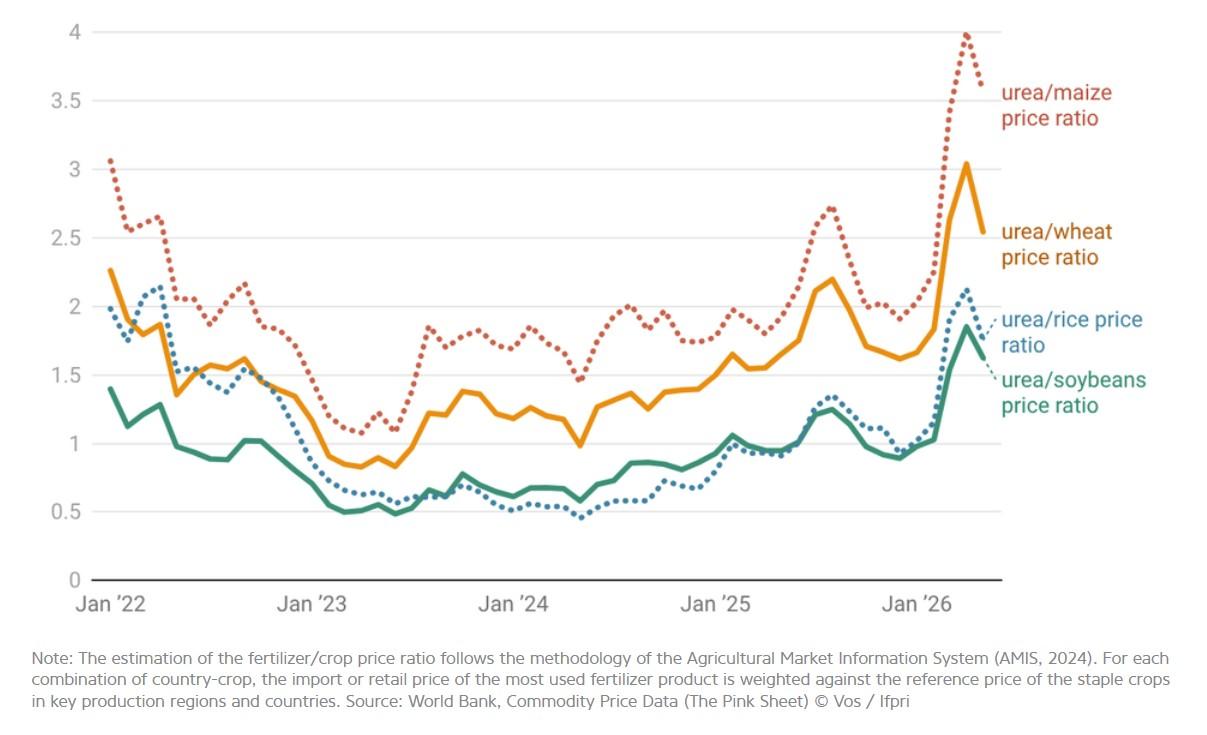

Second, higher costs may translate into lower fertilizer use, affecting yields. This risk is high for the upcoming late summer and autumn planting seasons. So far, staple food prices have not risen along with input costs, causing a sort of “affordability crisis” for farmers. Figure 3 shows the relative international price of urea with respect to the international prices for rice, wheat, maize and soybeans. An increase in this fertilizer/crop price ratio suggests inputs have become less affordable, affecting farm profitability.

Figure 3 Affordability crisis for farmers: relative price of urea with respect to staple food prices, since 2022

Third, even if the conflict ends today (mid-June 2026) fertilizer markets would not return to normality before the end of 2026. A more pessimistic scenario, with a more prolonged conflict and continued restrictions on shipments out of the Strait of Hormuz, expects the fertilizer crisis could extend into 2028 (Arita et al. 2026).

Fourth, governments are stepping up efforts to limit impacts of lower fertilizer usage on food supplies. China’s decision at the end of May 2026 to lift its ban on urea exports may further help curb the initial surge in world market prices. The U.S. Department of Agriculture has taken steps to boost domestic fertilizer production and revived a program to support farmers adopting practices that reduce the need for chemical fertilizer use. However, it may take a year or longer before this has an impact on fertilizer prices. Similarly, the EU’s Fertiliser Action Plan (EU 2026) aims to both boost fertilizer production and promote fertilizer-efficient farming practices, including targeted financial support to farmers to mitigate rising input costs and supply shortages. Low- and middle-income countries (LMICs) traditionally rely on input subsidies, but compensating farmers for the steep price rise in fertilizer markets would come at a likely prohibitive fiscal cost to most governments, especially those in Sub-Saharan Africa.

Protecting farmers from price volatility will require considerable future investments for alternatives like biofertilizers and fertilizer-saving farming practices, like conservation agriculture. Many farmers therefore will have to ride through the storm of higher input prices during 2026 hoping that governments will sustain their support for more sustainable farming practices that will lower their dependence on chemical fertilizers and fossil fuels.

The impact on consumers and the poor

In wealthier countries, the cost of farming is a small part of the final price of food, so higher farm costs do not immediately lead to more expensive groceries. Energy and shipping costs eventually work their way through the system, but it can take three to six months for these higher costs to show up in store prices, and once they do, they can last for 12 to 18 months after the initial increase. Rising energy prices also risk lowering food quality and safety, especially if it becomes harder to keep food cold or process it safely.

Since the conflict started, global consumer price inflation has accelerated notably, reflecting higher energy and transportation cost. The general consumer price index (CPI) in high-income economies has risen by approximately 2.5% since the beginning of the conflict, contributing to an annual increase near 4.2% (OECD 2026; IMF 2026). The CPI in LMICs has risen by an estimated 3.6% since the conflict started, pushing annual inflation rates to an average of 7.8% during April 2026.

The burden of higher consumer prices will be distributed unevenly. They will be felt the most by those nations and consumers who are least equipped to handle rising costs. Households in low-income countries spend around 50% of their income on food. This means that if food prices rise by 10%, their disposable income drops by 5%. On the other hand, families in high-income countries use a much smaller portion of their income for food, so price increases have a far lesser effect on their finances. In other words, supply chain disruptions and rising prices hit hardest those with less purchasing power and weaker social protection systems.

Low-income countries that rely on food imports face an added challenge known as the “dollar double-whammy.” Not only do global commodity prices go up in U.S. dollars, but geopolitical instability often makes the dollar even stronger. As a result, when these countries convert import costs into their local currencies, the prices become even higher, stretching budgets and making food less affordable.

With declining food supplies there is also the risk that major food-producing countries restrict their exports to protect their own domestic supply, as they have done during previous global food price shocks (Martin et al. 2024). These restrictions reduce the amount of food available globally and speed up price increases, hitting import-dependent countries the hardest.

Humanitarian supply chains are directly under pressure. According to the latest Global Report on Food Crises, nearly 300 million people were facing high levels of food insecurity and were in need of food assistance in 2025 (GNAFC 2026). Their situation will worsen, as rising fuel and commodity prices diminish the purchasing power of already much diminished aid budgets. As a result, less food can be distributed, making vulnerable groups more food insecure.

A global food price crisis could still emerge if the Iran war drags on despite all efforts at negotiations. However, if hostilities end in the coming weeks and shipments can flow freely again through the Strait of Hormuz, it is unlikely that there will be a global food crisis for everyone.

But for many poor households the crisis will erode purchasing power and their access to food. It will hurt farmers through constrained access to farming supplies and it will weaken humanitarian support for the hundreds of millions already facing high levels of acute food insecurity and malnutrition.

References:

AMIS (2024) AMIS fertilizer/crop ratio. AMIS Market Monitor Background Note No. 2. Rome: Agricultural Market Information System.

AMIS (2026a) Agricultural Market Monitor, June 2026. Rome: Agricultural Market Information System.

AMIS (2026b) Hormuz shock: global and regional impacts on fertilizer markets. Rome: Agricultural Market Information System.

Arita, Shawn, Wang, Ming, Kim, Jiyeon, Chakravorty, Rwit, and Steinbach, Sandro (2026). Strait of Hormuz Disruption Scenarios and Fertilizer Purchasing Risks for U.S. Crop Producers. Agricultural Risk Policy Center, North Dakota State University. farmdoc daily (16):75 (April 29).

European Commission (2026). Fertiliser Action Plan: Partnership for ensuring the availability, affordability and strategic autonomy in home-grown EU fertilisers. COM(2026) 310 final. Brussels: European Commission.

GNAFC (2026) Global Report on Food Crises 2026. Rome: Global Network Against Food Crises and Partners.

Hebebrand, Charlotte, Glauber, Joseph, Vos, Rob, and Rice, Brendan (2026). The Iran war’s impacts on global fertilizer markets and food production. IFPRI Blog. April, 1.

IMF (2026) IMF World Economic Outlook. April 2026: Global Economy in the Shadow of War. Washington D.C.: International Monetary Fund.

Martin, Will, Mamun, Abdullah, Minot, Nick, and Vos, Rob. 2024. Trade policy and food price volatility: Beggar thy neighbor or beggar thyself?IFPRI Blog Research Post. June 7.

OECD (2026). OECD Economic Outlook, Volume 2026 Issue 1. Paris: Organization for Economic Development and Cooperation (June, 3).

Vos, Rob, Glauber, Joseph, Hebebrand, Charlotte, and Rice, Brendan (2025). Global shocks to fertilizer markets: Impacts on prices, demand and farm profitability. Food Policy 133 (102790).