India’s new ban on rice exports: Potential threats to global supply, prices, and food security

On July 20, India announced that it would restrict exports of non-basmati rice to calm domestic rice prices that had risen more than 30% since October 2022 (Figure 1). The ban would halt overseas sales of the grain with “immediate effect,” the government announced, and is estimated to cover about 75%-80% of Indian rice exports.

The ban is the latest blow to the global rice market, whose prices have risen 15%-20% since September 2022—this coming after a period of relative stability in the earlier part of that year, even as prices of other cereals were soaring due to the Russia-Ukraine war. Over the past 15 years, India has become the world’s largest rice exporter, accounting for 40% of global rice exports in 2022/23, so any move it makes can have significant market reverberations.

India’s current move adds to its earlier, more limited export restrictions on rice. In 2022, India implemented a ban on the export of broken rice and imposed a supplemental tariff of 20% on exports of non-basmati rice. Yet India rice exports still totaled a record high 22.3 million metric tons in calendar year 2022. But the latest ban may send those numbers falling, posing risks of higher global prices and heightened food insecurity.

Figure 1

The new trade restriction threatens already vulnerable global rice markets. In a previous post, we discussed how a strengthening El Niño could reduce South and Southeast Asian rice production. While current crop forecasters continue to project normal yields assuming normal weather patterns, a delayed or truncated monsoon this summer could lower rice yields and increase demand for imports at the same time the world’s largest exporter is restricting supplies to the rest of the world. This post assesses India’s key role as a global rice exporter and potential impacts of the rice ban.

India’s growing presence in the global rice market

India emerged as the world’s largest rice exporter only in the last 10 years. Historically poor yields and production meant that India was a net rice importer through most of the 1960s and early 1970s (Figure 2). By the late 1970s, India had largely achieved self-sufficiency, and by the early 2000s had become a net rice exporter. Since 2010, rice production has increased by 40% (by over 40 million tons, to a grand total of 136 million tons, making it the second largest producer after China’s 146 million tons). India’s exports over the same period rose by 20 million tons. (China’s rice exports are a fraction of India’s.)

Figure 2

As a result, India has been the largest global rice exporter since 2014/15 (Figure 3). Over the past four years, its market share has averaged over 40%.

Figure 3

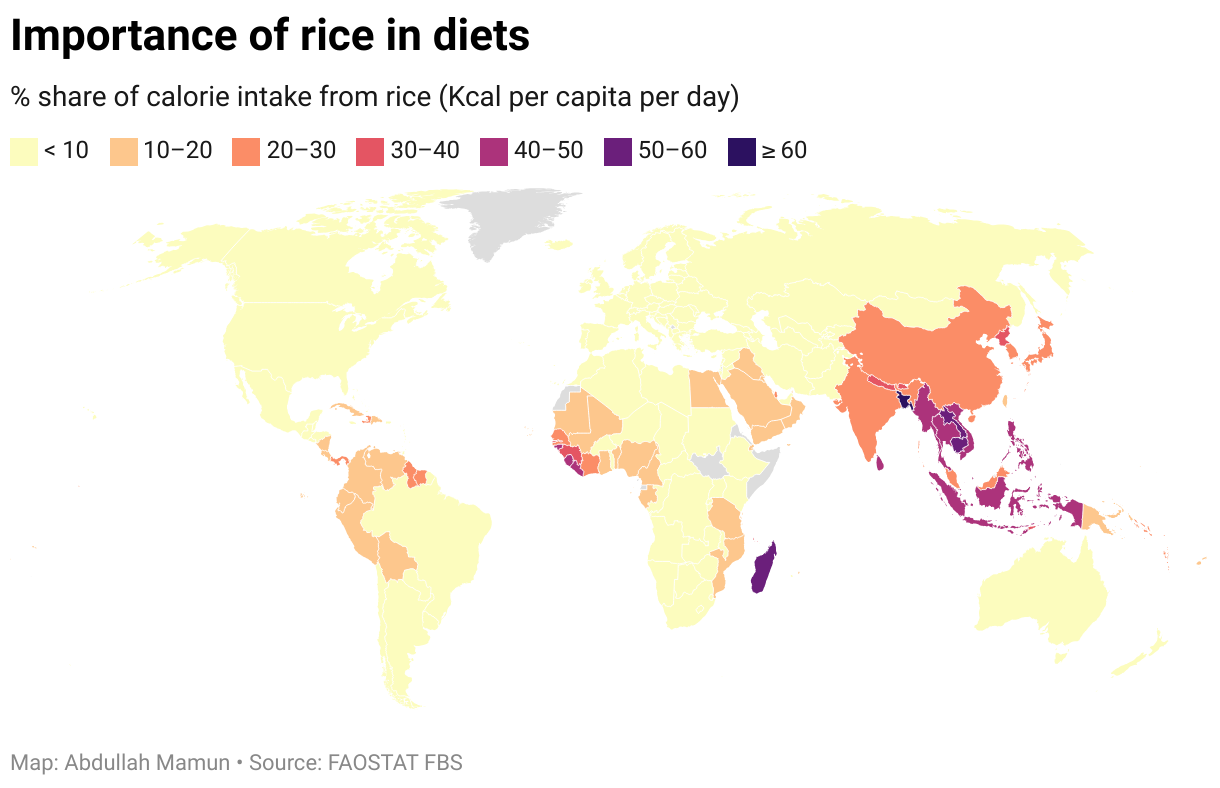

The importance of imported rice in country diets

Rice is one of the most widely consumed cereals in the world, and accounts for a large share of caloric consumption in many countries, particularly in South and Southeast Asia and in some countries in Africa (Figure 4).

For example, in Asia, the share of rice consumption in total calorie intake a day in some of the top consuming countries—including Bangladesh, Bhutan, Cambodia, Indonesia, Myanmar, Nepal, Thailand, the Philippines, and Sri Lanka—ranges from 40% to 67%, according to the UN Food and Agriculture Organization. Importantly, many of these countries—including Bangladesh, Bhutan, China, Sri Lanka, and Nepal—import a significant portion of their rice from India. Much of the rice consumed outside of Asia is also imported.

Figure 4

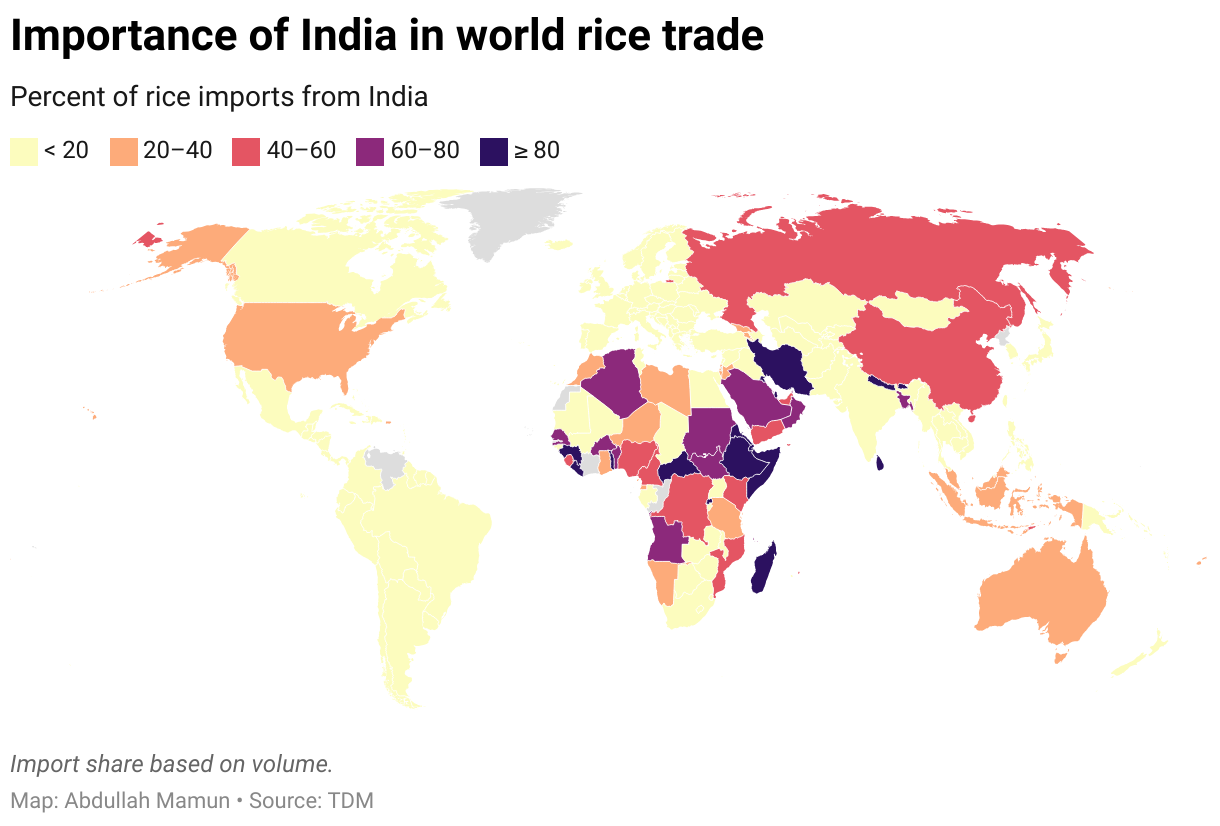

Where are India’s markets?

India is a major supplier to rice to several important markets in Asia and Sub-Saharan Africa (Figure 5), making their populations vulnerable to rice market disruptions. Forty two countries get more than 50% percent of their total rice imports from India, a significant share not easily substituted with imports from other large exporting countries such as Viet Nam, Thailand, or Pakistan. In Africa, India’s market share in 2022 exceeded 80% for several countries.

Figure 5

India and export restrictions

India’s latest export ban may not come as a surprise. The IFPRI export restrictions tracker shows that India has often imposed export control measures during periods of high global prices. During the 2007-08 and 2010-11 food price crises India banned export of rice, mostly non-basmati rice, for extended periods. With global markets disrupted by Russia’s invasion of Ukraine starting in February 2022, India initially imposed a wheat export ban, fearing domestic inflation and rising import demand from the rest of the world, then the limit on exports of 5% broken rice and the 20% export levy on unmilled and husked rice (both likely to continue through 2023).

Likely impacts of the ban

What effects will India’s ban have on world rice prices? That depends on several factors.

The first factor is the question of how stringent the export restrictions will be. India’s 2022 ban on wheat exports initially triggered a spike in global wheat prices, but as it became more clear that India would continue to honor existing letters of credit for wheat purchases and that it would keep selling wheat to neighboring countries for humanitarian purposes, prices retreated. India wheat exports in calendar year 2022 achieved record levels, though volumes dropped off considerably by the end of the year.

If India continues to allow sales of non-basmati rice to neighboring countries, or if the ban proves temporary, the market impacts may be limited. But a “hard” ban could have large implications for countries currently dependent on imports from India. Compared to other grains, rice is relatively thinly traded in global markets. Rice exports account for about 11% of total global production, compared to 16% for maize, 27% for wheat, and 42% for soybeans. Thus a ban affecting 40% of global rice exports would put pressure on other suppliers and on rice inventories—which have been drawn down in recent years, but would be needed to buffer price impacts.

The second factor is whether the strengthening El Niño and the positive Indian Ocean Dipole will diminish the summer monsoon season, lowering rice production in India and other countries in South and Southeast Asia. Continued normal rice yields would significantly reduce pressures in India to maintain an export ban to meet domestic needs. But poor rice crops in India and other major exporters like Thailand and Viet Nam would greatly lower world market supplies, reinforcing the rationale behind the ban.

The third factor is the degree to which India’s actions might spread to other rice exporting countries.

The unfortunate lesson from the food price spikes of 2007/08 was that once a few major rice exporters imposed bans, other rice exporters followed suit. Viet Nam imposed restrictions in June 2007 and India followed in October 2007, and by May 2008, Pakistan and Thailand had also joined. The combined market share of those four countries was over 70%. From October 2007 to April 2008, the benchmark Thai rice price almost tripled (Figure 6).

Figure 6

If other countries follow India’s export ban on non-basmati rice and impose their own export restrictions, the global market will presumably react sharply. Bangladesh, having the highest dependency on rice consumption in calorie intake and also being India’s largest rice trading partner, is closely monitoring the trade policies of its neighbor. Other South Asian neighbors would also be impacted by additional export bans on rice; while export duties on broken and other non-basmati rice would also exacerbate the situation.

Conclusions

India’s decision to ban exports of non-basmati rice varieties creates a new vulnerability in commodities markets that threatens already tenuous global food security. Many factors, from atmospheric conditions in the coming weeks, to the exact details of the export ban, to the reactions of other rice exporters, will determine what happens and how severe the ramifications are. We hope that the lessons of previous price spikes—which had lasting impacts on global hunger, food insecurity, nutrition, and poverty—will play a role in trade policy decision-making and deter countries from going down the path of imposing export restrictions.

Joseph Glauber is a Senior Research Fellow with IFPRI's Markets, Trade, and Institutions (MTI) Unit; Abdullah Mamun is an MTI Senior Research Analyst. Opinions are the authors'.