Will the Iran crisis lead to another round of food price spikes?

Key takeaways

- Fertilizer and energy, not food, are the core shocks. The Hormuz closure is disrupting energy and fertilizer shipments and driving up prices, but grain markets remain stable.

- Classic food price‑spike conditions are absent. Strong demand, tight stocks, weak dollar, and weather shocks aren’t aligning as in past crises.

- Food prices likely won’t surge soon. Ample global stocks and favorable crop conditions limit the risk of broad commodity price spikes.

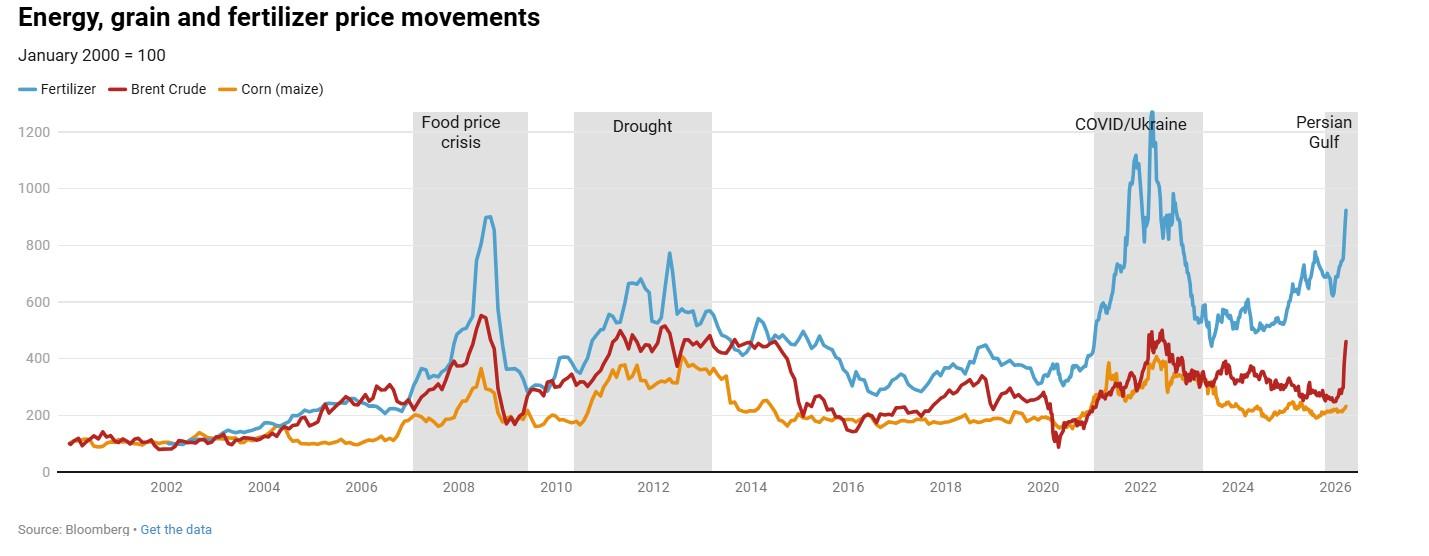

Agricultural commodity prices have been under sustained downward pressure since 2013–14. The 2022 spike in the wake of COVID-19 disruptions and Russia’s invasion of Ukraine proved temporary rather than cyclical. Now, the Strait of Hormuz closure amid the Iran war has produced a sharp run-up in fertilizer prices, raising agricultural production costs. Yet thus far, global commodities markets have not spiked. More than a month into the crisis, urea prices are up roughly 40%, while wheat and maize prices have increased by about 6% and soybeans less than 3%). Rice prices have fallen over the period.

Are we at the beginning of another period of high food prices? The short answer, in our assessment, is probably not—at least not yet. The conditions that drove prior price spikes are largely absent today, and the Hormuz disruption is a fundamentally different kind of shock than either the 2007-2008 food price crisis or 2022. The Hormuz disruption is a fertilizer supply shock, not a crop supply shock, and that distinction matters both in price formation and appropriate policy responses.

During previous agricultural price spikes, including 2007-2008, 2010-2012, and 2021-2022, energy, fertilizer, and grain prices moved together: rising and falling in tandem (Figure 1). In 2026, the pattern is different: fertilizer and energy prices are rising while grain prices remain roughly flat.

Figure 1

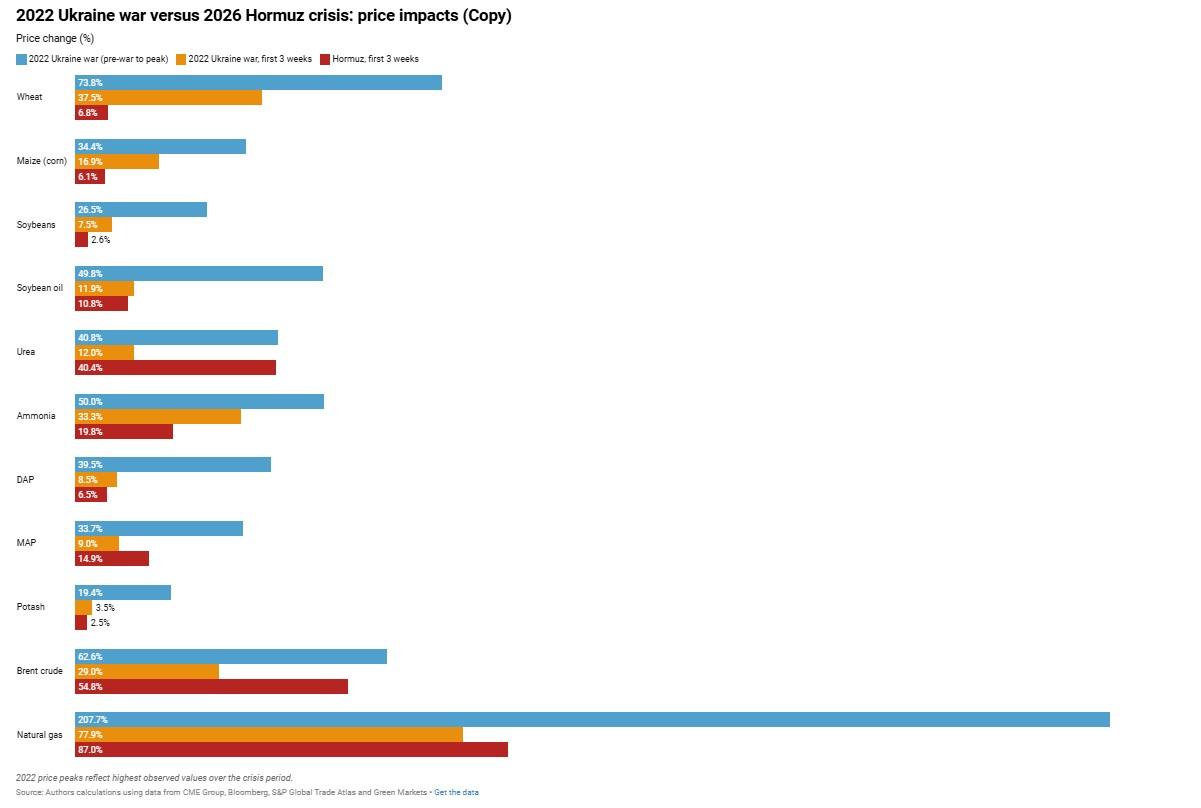

Comparing the Hormuz disruption to the war in Ukraine

The Russia-Ukraine war offers a clear illustration of how the current crisis differs from past food price shocks. Before the February 2022 invasion, Ukraine accounted for roughly 16% of global corn exports and, together with Russia, 29% of wheat exports. The conflict disrupted both grain supply and fertilizer supply from the region simultaneously. Crop prices surged alongside input costs, which partially offset the margin impact for farmers. With maize prices at $235-$275 per metric ton (MT), fertilizer prices at $1,000/MT were costly but manageable.

Figure 2

The Persian Gulf crisis presents a fundamentally different picture. The Gulf states export virtually no grain to the world market. What they do supply is fertilizer—and on a larger scale than Russia and Belarus combined. The Gulf accounts for a significant share of global urea, phosphate, and ammonia trade. Saudi Arabia alone supplies roughly 55% of U.S. ammonium phosphate imports. The major fertilizer producers in Qatar (QAFCO) and Saudi Arabia (SABIC Agri-Nutrients) have declared force majeure and temporarily stopped production of urea.

Iran’s shutdown of most cargo traffic through the Strait of Hormuz has resulted in ships stacked up, awaiting passage that may or may not come anytime soon. As of mid-March, Kpler vessel tracking identified 23 fertilizer vessels loading or laden in the Gulf with transit status uncertain. Nikkei Asia reported 21 ships carrying nearly one million MT of fertilizer were stuck in the Gulf awaiting transit of the Strait.

The 2026 disruption may ultimately prove more severe on the fertilizer side than 2022. Then, Russian fertilizer volumes dipped sharply in the first half of the year before recovering as trade rerouted through Brazil, India, and China. Russian volumes largely recovered by 2023 and reached record levels in 2024. Belarusian potash exports, however, fell by roughly 50% and did not fully recover. In 2026, the physical closure of the strait is a hard constraint: product is manufactured but has no ocean exit. If the strait remains closed and production disrupted for an extended period, fertilizer prices could exceed the 2022 records.

For producers, current maize prices of $155-$165/MT—roughly 40% lower than in 2022—make high diammonium phosphate (DAP) prices of $700/MT-$750/MT far less affordable than they were in 2022. Fertilizer-to-crop price ratios were already at historically poor levels before the Hormuz crisis began. This is the core of the asymmetry: in 2022, high crop revenues helped absorb high input costs. In 2026, that offset does not exist. The deteriorating fertilizer-to-crop price ratio may have potential implications for food production and food security, but at least in the short term, rising food prices are not among them.

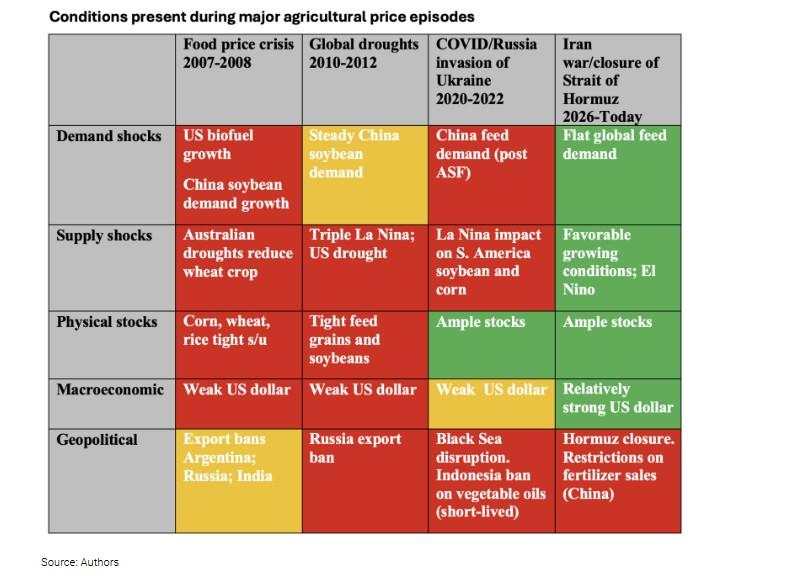

Historical precedents: What drove prior price spikes?

To assess whether 2026 is likely to produce another sustained period of high agricultural commodity prices, it is useful to examine the conditions that preceded prior price spike episodes. We consider four episodes—the 2006-2008 food price crisis, the 2010-2012 droughts in the Black Sea and North America, the 2021-2022 COVID and Ukraine shock, and the current Hormuz disruption—across five dimensions: demand, supply, stocks, macroeconomic conditions, and geopolitical factors (Table 1). The individual cells in the table are color-coded: red indicates that the factor has a strong positive impact on prices and green, a negative impact. Overlapping, multiple shocks are generally correlated with larger price impacts.

Table 1

The pattern is clear: the two largest and most sustained price episodes (2007-08 and 2020-22) occurred when multiple reinforcing conditions were present simultaneously. In 2007-08, structural demand growth from U.S. biofuels and Chinese protein consumption coincided with Australian drought, tight stocks across multiple crops, a weak dollar, and a wave of export restrictions. In 2020-22, several factors all converged within an 18-month window. A strong La Niña event reduced maize and soybean yields in Brazil. China’s recovery following an outbreak of Asian swine flu (ASF) increased its demand for imports of animal feed. These came on top of the Ukraine invasion and a weak dollar.

In 2026, only one column is red: the geopolitical row. The other four conditions are either absent or working against a sustained price increase. The following subsections assess each in turn.

Demand shocks

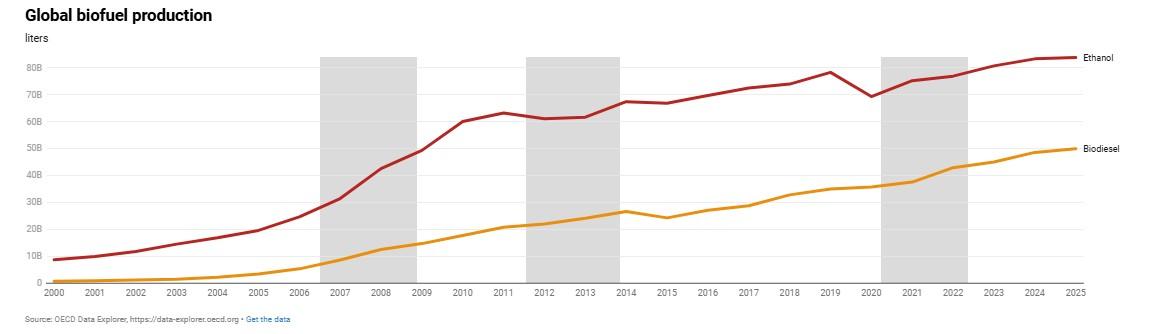

The 2007-2008 food price crisis was driven in large part by the U.S. mandate requiring minimum levels of ethanol in fuels, which created roughly 100 million MT of new annual maize demand (Figure 3). By 2011, that structural shift had been absorbed—U.S. ethanol production plateaued after 2010. Today, global biodiesel and ethanol volumes are growing, but this represents incremental demand, not a step-change comparable to the U.S. ethanol surge of 2006 to 2011.

Figure 3

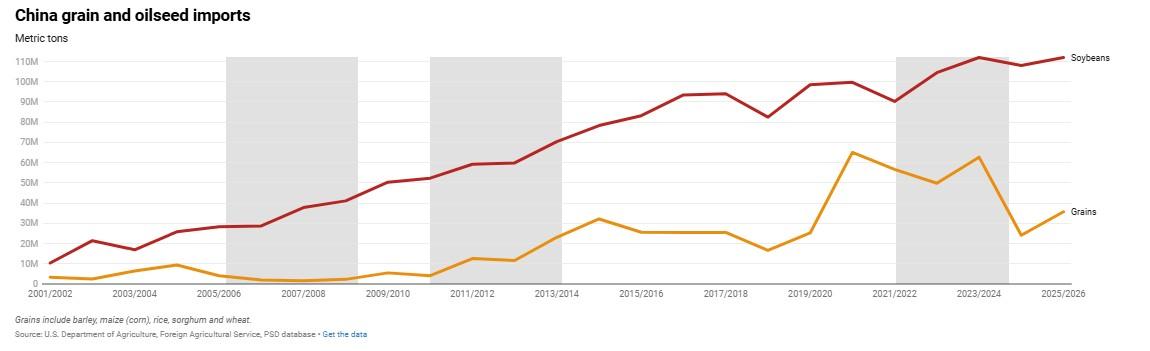

China has been the major driver in global import demand for both oilseeds and grains over most of the last 25 years, but that growth has begun to flatten in recent years (Figure 4). From 2005 to 2015, driven by dietary transitions and growth of domestic animal production, China soybean imports more than tripled, growing over 11% annually. This growth was temporarily halted by the ASF outbreak in 2018 which led to the herd culling of 250 million pigs and reduced feed demand. But as herds were rebuilt in 2020 and 2021, soybean and feed demand grew sharply. Since 2022, soybean imports have flattened and feed grain imports have largely collapsed as domestic production expanded by roughly 40 million MT. Soybean imports have plateaued near 100-110 million MT.

Figure 4

Supply shocks

Supply shocks had a large role in the prior price spike episodes of 2007-2008 and 2010-2012. Successive droughts in Australia in 2006/2007 and 2007/2008 and poor harvests in North America contributed to a very tight wheat market. Drought in 2012 in North America, combined with a poor Brazilian soybean crop, resulted in record high soybean and maize prices. Likewise, the Ukraine war came on the heels of a poor North American spring wheat crop.

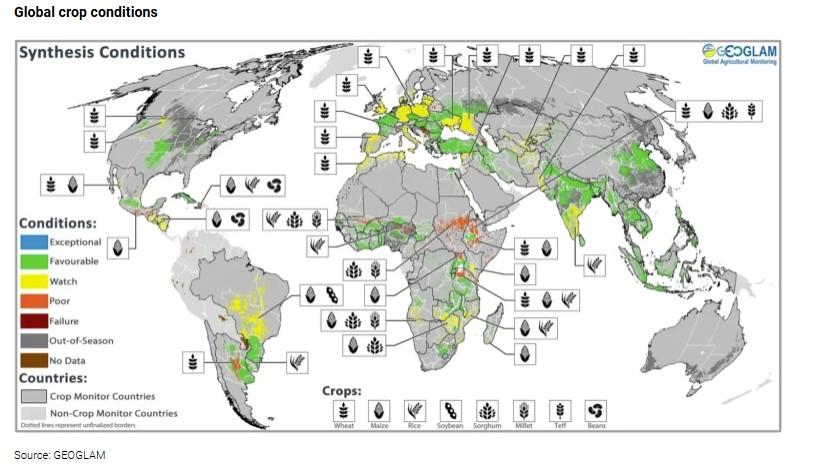

By contrast, early-season crop conditions for the upcoming growing season in the Northern Hemisphere look favorable. In its latest Crop Monitor, GEOGLAM rates 17 of 22 major region-crop pairs as favorable or exceptional (Figure 5). The U.S. National Oceanic and Atmospheric Administration reports a 62% probability of an El Niño event developing by mid-2026. Historically, El Niño events have significantly affected wheat, maize, rice, and soybean yields on every continent, although the impact is not always negative, and yield impacts in one region (e.g., South American maize production) may be offset by yields in another region (e.g., North America). At this point, yield impacts are very much uncertain, as much will depend on the duration and strength of the El Niño event.

Figure 5

Global stocks

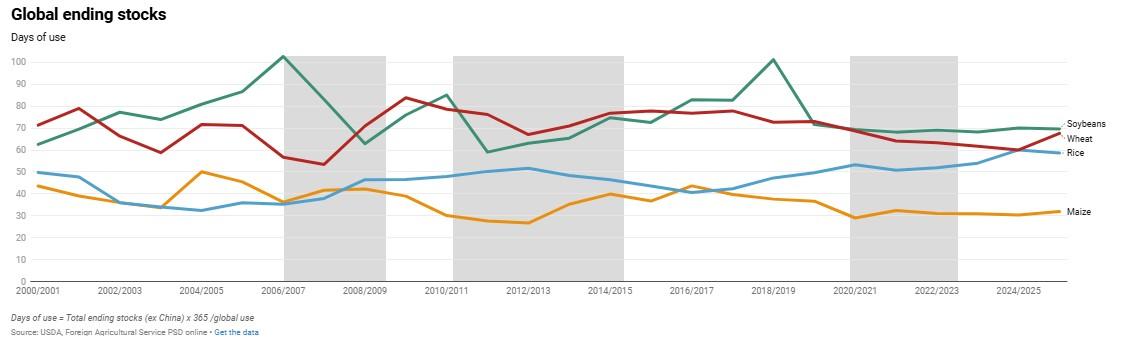

Another distinction between previous price spikes and the current situation with the closure of the Strait of Hormuz is that global commodities stocks are not at levels historically associated with sustained price rallies. Excluding China stocks (which are large but generally not exported), maize is the tightest of the four crops. currently considered at roughly 30 days of use, down from about 45 days in 2018/19—a meaningful decline, since maize cultivation is most exposed to weather impacts. Soybeans are near their long-run average. Wheat stocks are comfortable. Rice reserves, while declining modestly, remain well above historical crisis levels.

Figure 6

The relative strength of the U.S. dollar

Each of the three prior rallies coincided with a weak dollar. The nominal broad dollar index (DXY) hit its all-time low of roughly 71 during the 2007-2008 food price crisis, fell to about 73 during the 2010- 2012 drought rally, and troughed near 89 in 2021 just prior to the surge of prices in the second half of 2021 and 2022. The dollar strengthened relative to other currencies from 2021 through late 2024 and despite declining somewhat in 2025, the DXY currently sits near 99-100. A weak dollar tends to be strongly correlated with higher commodity prices, in part, due to the fact that internationally-traded commodities are dollar-denominated. A sustained weakening of the dollar would be among the most powerful catalysts for a rise in commodities prices, but there is no clear indication of one at present.

Figure 7

Government policies that exacerbate price spikes

In prior commodity price episodes, export restrictions amplified price spikes in grain markets. In 2026, the same dynamic is operating in fertilizer markets, and on a larger scale.

The mechanism is familiar from the food price crises of 2007-08 and 2010-11. When a major exporting country restricts outflows to protect domestic consumers, the supply available to the world market contracts, prices rise further, and other exporters face pressure to impose their own restrictions.

In 2007-08, cascading export restrictions and other insulating trade policies—imposed by more than a dozen countries including India, Viet Nam, Egypt, China, Russia, Argentina, Ukraine, and Kazakhstan — accounted for an estimated 45% of the increase in global rice prices and roughly 30% of the wheat price increase. In 2010-11, Russia imposed a grain export ban from August 2010 through July 2011, removing an estimated 14-15 million MT of wheat from the export market, though the extreme drought that year would have reduced exports substantially even without the ban. In neither case did the restrictions reduce global production—they simply redirected supply from the international market to domestic use, amplifying price volatility for import-dependent countries.

In 2026, it is fertilizer, not grain, that faces this cascading restriction dynamic. Grain prices are near the cost of production and no major exporter has imposed or signaled grain export bans. The kind of food price spike that defined 2007-08 and 2022 is not materializing. But the fertilizer market is experiencing something arguably worse: a sustained, multi-year tightening of export availability from China, the world’s largest producer, compounding the physical supply disruption in the Persian Gulf.

China’s fertilizer export restrictions are qualitatively different from the grain export bans of prior episodes. Those were reactive, imposed after prices had already spiked, and typically reversed within months. China’s controls have been in force, in escalating forms, since mid-2021. What began as an informal administrative guidance in July 2021 was formalized in October 2021 through mandatory customs inspection requirements giving authorities discretion to delay or block exports indefinitely.

Since then, China has alternated between near-total export freezes and tightly managed quota windows, with the overall trajectory toward greater restriction. From 2021-2024, Chinese urea exports collapsed from approximately 5.3 million MT to under 300,000 MT—a 94% drop. DAP exports, which averaged roughly 6.3 million MT annually during the unrestricted 2019–2021 baseline, have fluctuated sharply under the restriction regime—falling to approximately 3.6 million MT in 2022, partially recovering under quotas in 2023, and declining again in subsequent years. In December 2025, China effectively suspended phosphate exports through August 2026, citing surging domestic prices and the need to secure spring planting supply. In March 2026, the ban was broadened to include nitrogen-potassium fertilizer blends for the first time. As of late March 2026, only ammonium sulfate and a handful of specialty products remain available for Chinese export.

The interaction between China’s restrictions and the Hormuz closure is the critical compounding factor for global fertilizer markets. Under normal circumstances, Chinese phosphate and urea would be the natural alternative supply for markets cut off from Gulf production. With China largely out of the export market, for reasons entirely unrelated to the Gulf conflict, three of the five major global phosphate sources are constrained simultaneously: DAP production by Maaden, the Saudi state-owned mining company, is physically blocked behind the strait, Morocco’s OCP Group faces reduced sulfur and ammonia availability as Gulf sulfur supplies are disrupted, and China’s exports are suspended by administrative fiat. OCP retains partial operational capacity through alternative product lines and existing sulfur stocks, but its sulfur-dependent DAP and MAP output is constrained. This degree of simultaneous supply concentration is unprecedented in fertilizer market history and explains why fertilizer prices are spiking even as crop prices remain subdued.

Further complicating the situation, the policy response to fertilizer trade disruption has also been less coordinated in 2026 than it was for grain and fertilizer trade in 2022. In 2022, the international community made a deliberate effort to keep fertilizer flowing: The U.S. stated that Russian fertilizer was exempted from its economic sanctions, the EU carved out specific fertilizer exemptions from its sanctions packages, and the United Nations brokered the Black Sea Grain Initiative alongside a parallel memorandum of understanding with Russia to facilitate fertilizer exports. The UN Security Council has been debating measures which would reopen the Strait of Hormuz, but to date, members have not been able to reach agreement.

Russian fertilizer production and exports partially recovered by 2023, though ammonia exports remained constrained by the closure of the Togliatti–Odesa pipeline. In 2026, no comparable diplomatic effort to release Chinese fertilizer exports is underway, in part because China’s restrictions are framed as domestic food security measures rather than trade sanctions, and in part because international attention is focused on the military conflict itself. The result is that the policy space for mitigating the fertilizer price shock is narrower than it was in 2022, even as the underlying supply disruption is larger.

Growth of Southern Hemisphere production

Brazil’s agricultural expansion has fundamentally altered the dynamics of commodity price cycles. Its soybean production has tripled in two decades, from roughly 52 million MT in 2002/03 to a projected 180 million MT in 2025/26. Exports have grown proportionally. Brazil now accounts for approximately 60% of global soybean trade, up from about 33% during the 2006–08 crisis.

Brazil’s supply response capacity functions as a structural price ceiling. During the 2006–08 super-cycle, Brazilian agriculture was still scaling up and its supply response lagged by several years, contributing to price spikes. Today the response is faster and larger. Any sustained price increase induces Brazilian expansion within one to two planting seasons. Until, that is, something disrupts the Brazilian machine. Whether through La Niña drought, shrinking margins from rising input costs, or regulatory constraints such as the EU Deforestation Regulation (requiring certification that imports did not degrade forests), soybean and corn rallies are likely to be capped.

Conclusions

Despite the Iran crisis, current conditions remain more consistent overall with a late stage of a protracted period of low agricultural commodity prices rather than with the beginning of a new period of sustained high prices. The simultaneous conditions that powered previous price spikes—strong demand growth, tight stocks, a weak dollar, and weather-driven supply disruptions—are largely absent. Global food supplies remain ample across the major grains and oilseeds.

A prolonged Hormuz disruption has serious implications for global markets and the food system, but it is operating through a different channel than the previous price spikes. By raising fertilizer costs without raising crop revenues, it puts producers in a worsening cost-price squeeze. The fertilizer access question poses global food security challenges, particularly for low-income countries already stretched by the 2021-22 price spike, and deserves close attention. But it is not, in itself, a trigger for broad-based increases in global grain and oilseed prices.

However, the crisis still poses risks for key commodities.

Even under optimistic scenarios in which a ceasefire is reached, it will take time to reopen the strait fully: mine clearance, insurance reassessment, and logistics normalization are measured in weeks to months, not days. The supply-side damage to fertilizer production is already occurring: plants have shut down, force majeure declarations are in place, and sulfur and phosphate supply chains do not restart overnight. The fertilizer disruption will likely last for months after any end to hostilities.

Rice production could be vulnerable to an extended disruption in fertilizer supplies. Rice is fertilizer-intensive and concentrated in South and Southeast Asia, regions heavily dependent on Gulf urea imports. India, Pakistan, Bangladesh, and much of Southeast Asia source a significant share of their nitrogen fertilizer from Gulf producers. If higher fertilizer costs persist into the second half of 2026 and coincide with an El Niño event, rice-producing regions could face both rising input costs and less favorable growing conditions at the same time.

That said, higher fertilizer prices are likely to reduce fertilizer application at the margin rather than eliminate use; producers will apply less urea, but continue using it. Global rice reserves remain large. The production impact, while real, would likely be modest.

Wheat may also face some risks. Developing country wheat producers, particularly in North Africa, the Middle East, and Central Asia, also depend on imported fertilizer. FAO already projects a roughly 3% decline in global wheat production for 2026 on reduced sowings and localized weather stress. Further fertilizer cost increases could reinforce that decline. But global wheat stocks remain comfortable, well above levels associated with prior crises.

An escalation of the conflict beyond the strait, disrupting broader shipping lanes or triggering retaliatory actions affecting energy markets, would change the picture significantly. But under current conditions, the disruption remains primarily a fertilizer and energy problem, not a food supply problem.

Shawn Arita is Associate Director of the Agricultural Risk Policy Center at North Dakota State University; Joseph Glauber is a Research Fellow Emeritus with IFPRI’s Director General’s Office. Opinions are the authors.’