Increased tensions in Ukraine again threaten the Black Sea Grain Initiative

On June 6, the Nova Kakhovka dam in southern Ukraine, located about 70 km upstream of Kherson, a port city on the Dnipro River, collapsed, sending an uncontrollable flow of water from its reservoir downstream. Futures markets reacting to the news sent wheat futures up almost 3 percent before falling back later that day.

In an unrelated action, an ammonia pipeline, which prior to the war had carried anhydrous ammonia from Tolyatti in Russia to the Ukrainian port of Pivdennyi (Yuzhny) near Odesa, was reportedly damaged. While the pipeline had been inoperative since the start of the war, reopening it had been a condition put forward by Russia for extension of the Black Sea Grain Initiative during recent extension discussions.

What will be the impact of these developments? While the dam collapse and the damage to the ammonia pipeline are not likely to seriously affect grain supplies from Ukraine in the short term, increased tensions could result in termination of the Black Sea Grain Initiative.

Impact of the dam collapse

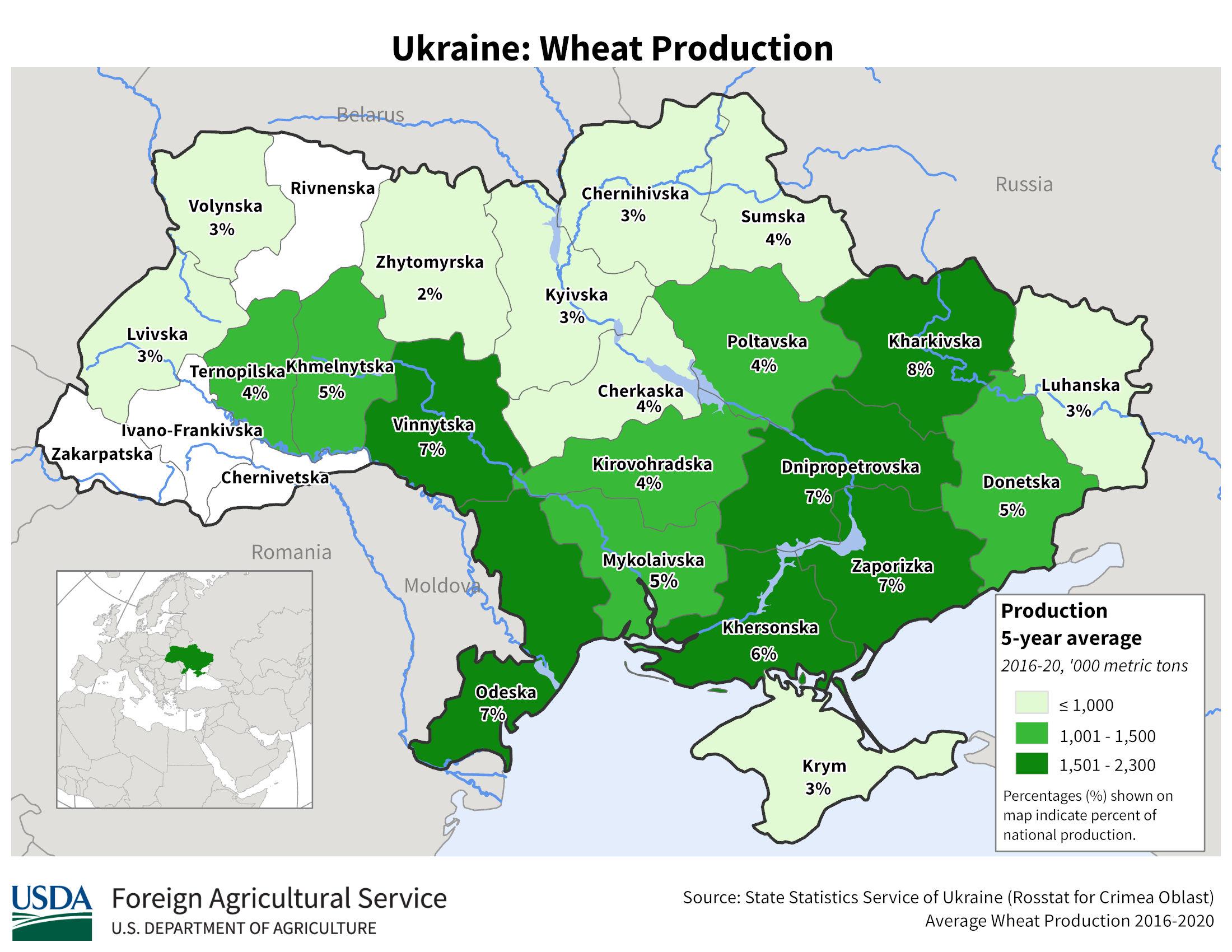

Over 2016–2020, Khersonska oblast (Kherson region) accounted for about 6% of total Ukraine wheat production (1.6 million metric tons), but the area immediately affected by the flooding, the lowlands along the Dnipro River, is far less productive (map). Earth observation data suggest that agricultural activity in the region had already been sharply reduced over the past year because of the war.

The long-term damage is less clear. Before its destruction, the Kakhovka dam and reservoir supported one of the largest irrigation systems in Ukraine and Europe, providing vital water resources to over 500,000 hectares of farmland. Much of this capacity was dedicated to the production of rice, potatoes, tomatoes, and vegetables. Irrigation has been recognized as a crucial factor in improving efficiency and profitability in the region’s agricultural production through increasing the proportion of high-value crops in the crop rotation. For this reason, the Ukrainian government had planned to modernize and expand the country’s irrigation systems since 2017, and the Kakhovka reservoir has been the foundation of these efforts. With this capacity now crippled for three to seven years, Ukrainian Agriculture Minister Mykola Solsky expressed concern that the loss of productivity could reduce income and investment among producers, ultimately affecting up to 1.5 million ha of farmland.

Figure 1

Damages to the ammonia pipeline

The ammonia pipeline is the world’s longest ammonia pipeline and has been inoperative since the Russian invasion in February 2022. Previously, most of Russia’s ammonia exports were transported through Pivdennyi as alternate routes were very expensive. As a result, Russian exports of anhydrous ammonia in 2022, calculated using data from reporting importers, were down 71% in volume compared to 2021.

As a condition of extending the Black Sea Grain Initiative, Russia has been demanding that Ukraine reopen the pipeline, but Ukraine has insisted that the pipeline was not part of the original agreement. The extent of the damage to the pipeline is not known, but in recent months, Russia has sought alternative outlets for its ammonia exports. Uralchem, Russia’s biggest potash and ammonium nitrate producer, plans to open a new specialized ammonia terminal in late 2023 on the Taman Peninsula in southern Russia.

Implications for the Black Sea Grain Initiative

The Black Sea Grain Initiative, a UN-brokered agreement between Russia and Ukraine, signed on July 22, 2022, has allowed Ukraine to export grain and other agricultural products that had been blocked since the Russian invasion in mid-February 2022. Under the agreement, Ukraine is granted safe passage for export ships from three key ports in the Black Sea: Odesa, Chornomorsk, and Pivdennyi, which accounted for approximately 37% of all Ukrainian agricultural exports prior to the invasion. The agreement has provided a vital path for exporting food from a critical global supplier. The deal has also provided assurances to Russia that food and fertilizer would not be affected by export sanctions, which is crucial as Russia is a major exporter of wheat and fertilizers. The initial agreement was signed for a period of 120 days and has since been extended multiple times, with the latest extension scheduled to expire on July 17, 2023.

As of June 9, over 31.5 million tons of agricultural products have been exported under the agreement, with 57% going to developing countries. Most of the exports consisted of corn (51%), wheat (11%), and sunflower oil (5%).

However, uncertainty looms regarding the extension and the implementation of the agreement. Russia's latest decision to restrict registrations at the Pivdennyi port, tied to the reopening of the ammonia pipeline, resulted in a decrease in the average daily inspection rate to 2.4 ships per day compared to over 5 earlier in 2023 and over 10 in September and October 2022. Exports out of Pivdennyi averaged 1.1 million tons per month from August 2022 to April 2023 and accounted for about one-third of total exports out of the Black Sea over the period. In May 2023, exports from Pivdennyi fell to about 100,000 tons and total exports out of the three ports fell to 1.3 million tons, the lowest level since the agreement went into effect (Figure 2).

Figure 2

Consequences of terminating the agreement

The impact of the closure of the Black Sea for Ukrainian exports has been discussed in much detail previously. Exporting overland through Eastern Europe is costly and limited by existing infrastructure. Moreover, increased exports from Ukraine to Poland, Hungary, Bulgaria, Romania, and Slovakia since February 2022 have increased costs of transportation and storage services and lowered prices in the region, thus creating tensions between Ukraine and its western neighbors. More exports from Ukraine, even if feasible, would only exacerbate these tensions.

The war has already caused significant declines in prices for Ukrainian wheat and other commodities (Figure 3), and further reduction of export volumes and increased export costs would lead to even lower prices and revenues for Ukrainian producers. While the opening of the Black Sea ports helped reduce the difference between other comparable wheat prices, that difference has grown again in recent weeks.

Figure 3

Lower prices mean reduced incentives for Ukrainian farmers to plant a crop. Exportable supplies of Ukrainian wheat and maize for the 2023/24 marketing year are almost 40% below 2021/22 levels. The termination of the Black Sea Grain Initiative would push these numbers even lower.

Conclusions

Within hours of the announcement of the signing of the Black Sea Grain Initiative in August 2022, the port of Odesa was struck by a rocket. Later in October, Russia briefly suspended its participation in the agreement, but rejoined days later. Despite Russia’s repeated threats to not renew the agreement, the deal has remained in effect for 10 months since its initial signing. While the outcome of the most recent events remains to be seen, there are hopeful signs that the agreement will hold again.

The Black Sea Grain Initiative provides enormous benefits both to traditional importers of Ukrainian grain and other foodstuffs, including many developing countries, and to global consumers through lower prices. The agreement is also critical for the long-term viability of the Ukraine’s agriculture sector. Its termination would have far-reaching consequences for global food security and agricultural supplies beyond the current crop year.

Joseph Glauber is a Senior Research Fellow with IFPRI's Markets, Trade and Institutions Unit (MTI); Brian McNamara is an MTI Program Coordinator; Elsa Olivetti is an MTI Research Assistant. Opinions are the authors'.