Staple Food Prices Generally Calm, But Rice, Coffee, Sugar See Volatility Rise

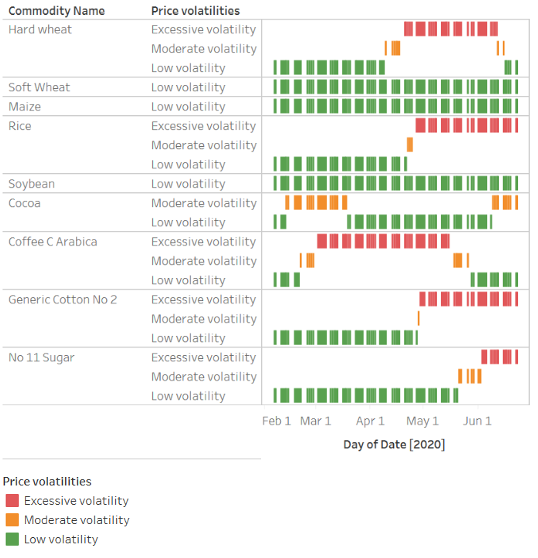

Futures prices for most staple food commodities have fallen since February because of market supply chain disruptions associated with the spread of the COVID-19 virus and lower oil prices, among other factors. However, overall, price variability in the major agricultural commodity markets has remained relatively calm in the face of COVID-19-related shutdowns. Until recently, the exceptions to this relative calm have included hard wheat and coffee. Hard wheat saw moderate and high levels of price variability from April 9 to June 15. This appeared to be related to tightening of wheat markets with lower stock-to-utility ratios, measures taken by two major wheat-producing countries (Kazakhstan and Russia) to limit exports, and reports of prospects of less favorable growing conditions in parts of Ukraine and other parts of Europe. Price variability in coffee was driven by low stock levels and supply disruptions, but these conditions calmed in the second half of May.

While wheat and coffee markets enter calmer waters, however, the Food Security Portal’s Excessive Food Price Variability Early Warning System is now showing high levels of price volatility in rice, cotton, and sugar markets. Rice has experienced 59 days in high variability, cotton 57, and sugar 22.

What might be behind these recent trends?

IFPRI’s COVID-19 Food Trade Policy Tracker indicates that Russia’s export bans on wheat are still in place but are set to expire at the end of June. As indicated in a recent USDA WASDE report, wheat prices may be calming due to projections that show high production levels in India, Australia, Turkey, and China, as well as improving crop prospects in the EU and Ukraine.

After a period of unusual fluctuations until mid-May, coffee prices have calmed mainly due to expectations of a larger 2020-21 Brazilian crop. In addition, lower global demand expectations have put an overall downward pressure on prices. The price of arabica coffee, which represents around 60 percent of globally traded coffee, has seen a particularly downward trend over the past month.

In the cotton market, COVID-19-related slowdowns in demand and associated high stock levels have pushed prices down. These high stock levels could keep cotton prices depressed even if demand increases as economies reopen. The recent variability in cotton prices is likely the result of uncertainties related to global demand for textiles and apparel amidst the current global recession.

As Bloomberg reports, Vietnam’s rice shipments increased 42% year-on-year in May to 953,950 tons, the highest level for the month since 2009. At the end of April, Vietnam ended its rice export ban. As one of the world’s major rice exporters, Vietnam’s absence from and reentry to the market could have implications for price stability. Moreover, fears of future export bans by other major exporters, as well as uncertainty about China’s next trade policy moves – as China controls a large percentage of global rice stocks – could be contributing to price variability in rice futures markets.

Sugar prices are especially sensitive to changes in crude oil prices due to the use of sugar in ethanol production. Oil prices have been highly variable due to COVID-19’s impact on economies, with subsequent impacts on the sugar market. Sugar prices have also been influenced by recovering oil prices and lower production levels in Thailand.

How the Excessive Food Price Variability Early Warning System Works

The Food Security Portal captures agricultural market variability through its Excessive Food Price Variability Early Warning System, which is updated on a daily basis. Through this system, price fluctuations in agricultural futures markets are closely monitored, and a timely measure of excessive price variability identifies periods of unusual price variability.

As regular users will have noticed, we have enhanced the tool to now monitor the degree of price variability in the markets for nine agricultural commodities (maize, hard wheat, soft wheat, soybeans, rice, coffee, cacao, cotton, and sugar), as well as for futures prices in energy markets (oil and natural gas) which often strongly correlate with agricultural prices.

Why should we be concerned with price variability?

Agricultural prices are inherently volatile and typically change every day. Yet high price variability may make it more difficult for farmers to make decisions about how and what to produce; make food processors and businesses more reluctant to invest in food and agriculture; promote speculative trading as larger price fluctuations create profit opportunities; and ultimately affect consumption decisions, particularly in rural areas that depend heavily on agricultural income. These consequences were felt in particular during the 2007-2008 global food price crises, during which the world witnessed a steep increase in the prices of staple foods followed by a period of high price variability. At the time, these increases came as surprise to many, creating a lot of uncertainty in food markets. The excessive price variability tool was developed precisely to provide early warning of unusual price movements and alert farmers, traders, investors, and policymakers of possible uncertain times to come.

Previous pandemics have caused food price spikes for various reasons. So far, there have been no visible signs of major food price spikes as a result of the COVID-19 pandemic and, as mentioned, world markets for main staple crops have remained relatively calm. In the case of COVID-19, impacts may remain muted for some time as, unlike with pandemics such as SARS, the avian flu, or MERS, the direct impacts of COVID-19 are not directly felt in the agricultural sector and producing areas. Furthermore, staple commodities can typically be loaded, shipped, and discharged with minimum human-to-human interaction. Finally, current levels of global reserves of non-perishable grains seem sufficient to meet any surge in demand. Should any of these conditions change, however, these shifts should be picked up immediately by the FSP’s excessive food price variability measure. This was the case for hard wheat and coffee earlier in the pandemic and now for rice, cotton, and sugar.

In the aftermath of the global food price and financial crises of 2007-2008, most staple food prices showed very high volatility until as late as 2012. Since then, world market prices for basic staples have been in relatively calm waters. But could this be silence before the storm? Monitor the situation through the Excessive Food Price Variability Early Warning System and join the Food Security Portal’s monthly newsletter for updates.

Rob Vos is Director of IFPRI's Markets, Trade and Institutions Division. Joseph Glauber and Manuel Hernandez are Senior Research Fellows with IFPRI's Markets, Trade and Institutions Division. Brendan Rice is a Research Analyst for IFPRI's Markets, Trade and Institutions Division.