September AMIS Market Monitor: Crop prices still falling; El Nino could be among strongest since 1950

Dropping oil prices, concern over the global financial implications of economic slowdown in China, and higher than expected global yields for wheat, maize and rice are all contributing to the continued descent of crop prices, according to the September edition of the AMIS Market Monitor and the FAO Food Price Index , both released today.

The AMIS Market Monitor represents the collective assessment of the ten international organizations that form the AMIS Secretariat concerning international market developments and outlook for wheat, maize, rice, and soybeans. Its coverage includes the world supply-demand, policy developments, international prices, and futures markets. The FAO Food Price Index is a measure of the monthly change in international prices of a basket of food commodities.

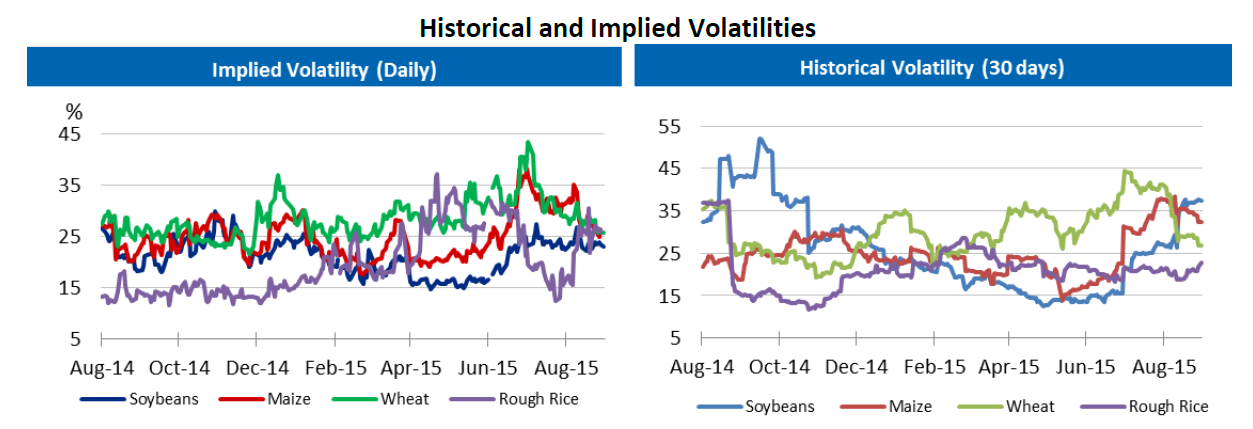

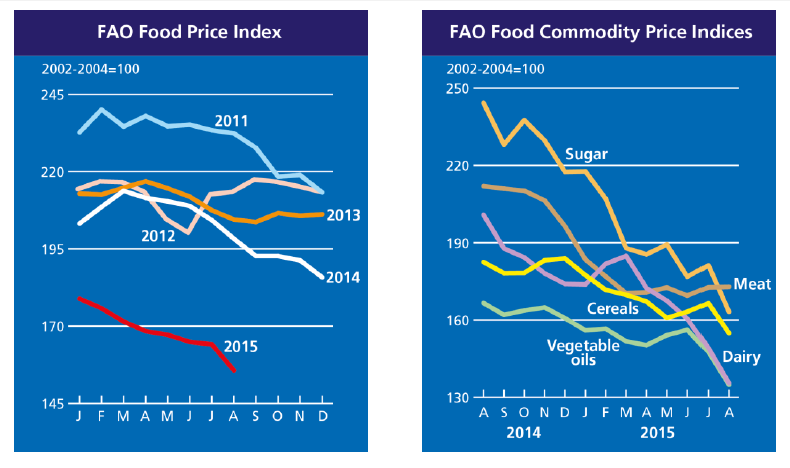

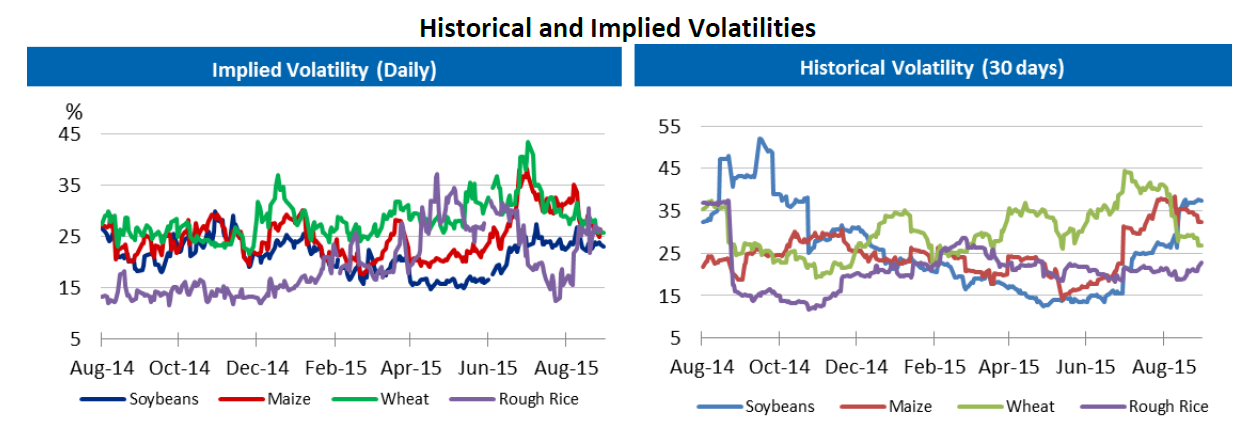

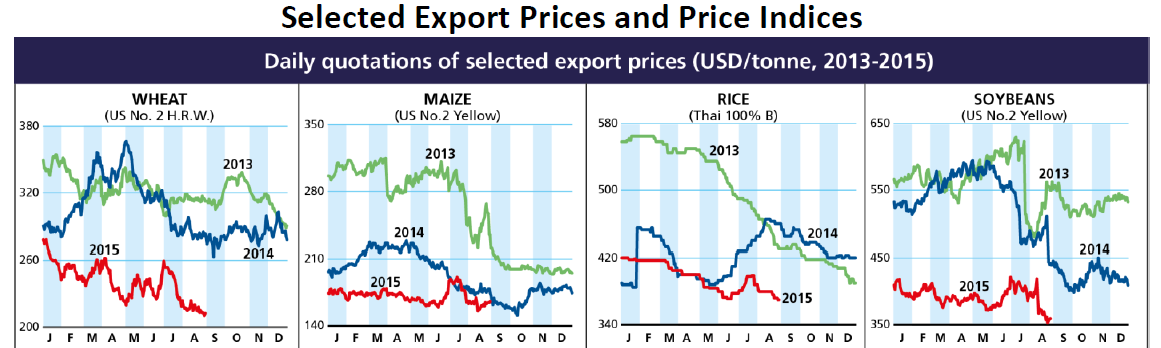

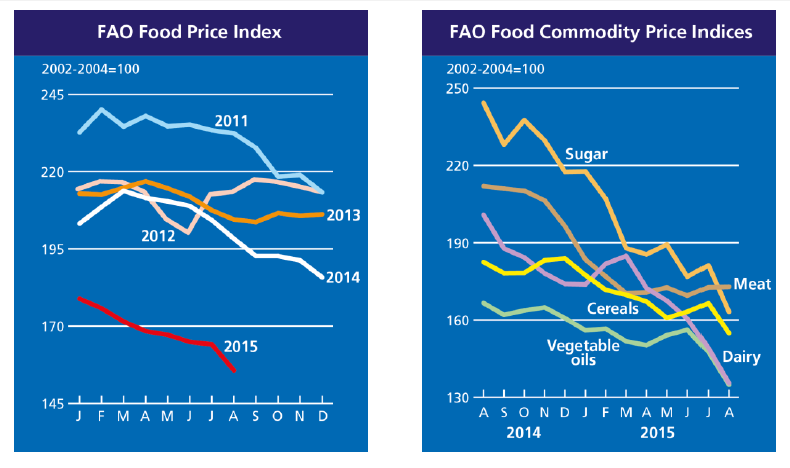

Sub-indeces of the International Grain Council (IGC) Grains and Oilseeds Index (GOI) showed a net decline of 9 percent m/m for wheat, 8 percent m/m for maize, 2 percent m/m for rice, and 5 percent m/m for soybeans (almost a quarter y/y). Historical Volatility registered in the low 30s, declining in wheat and rising in maize and soybeans. Volumes for wheat, maize and soybeans changed little m/m but were each higher y/y. The Food Price Index, which tracks prices for dairy, meat, sugar and vegetable oil in addition to wheat, maize and rice, averaged 155.7 points last month, down 8.5 points (5.2 percent) from July. All of the commodities tracked except meat experienced decline.

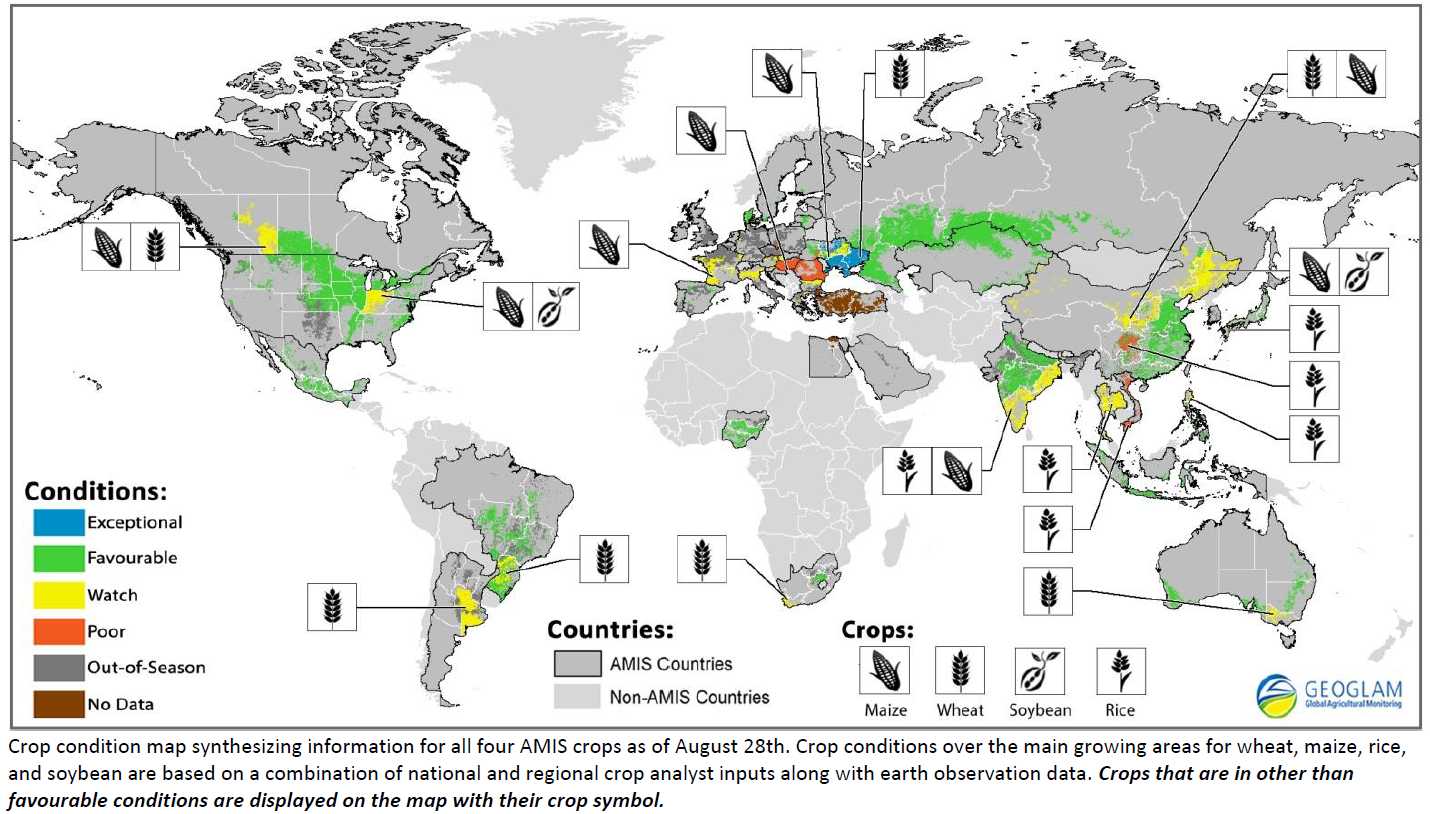

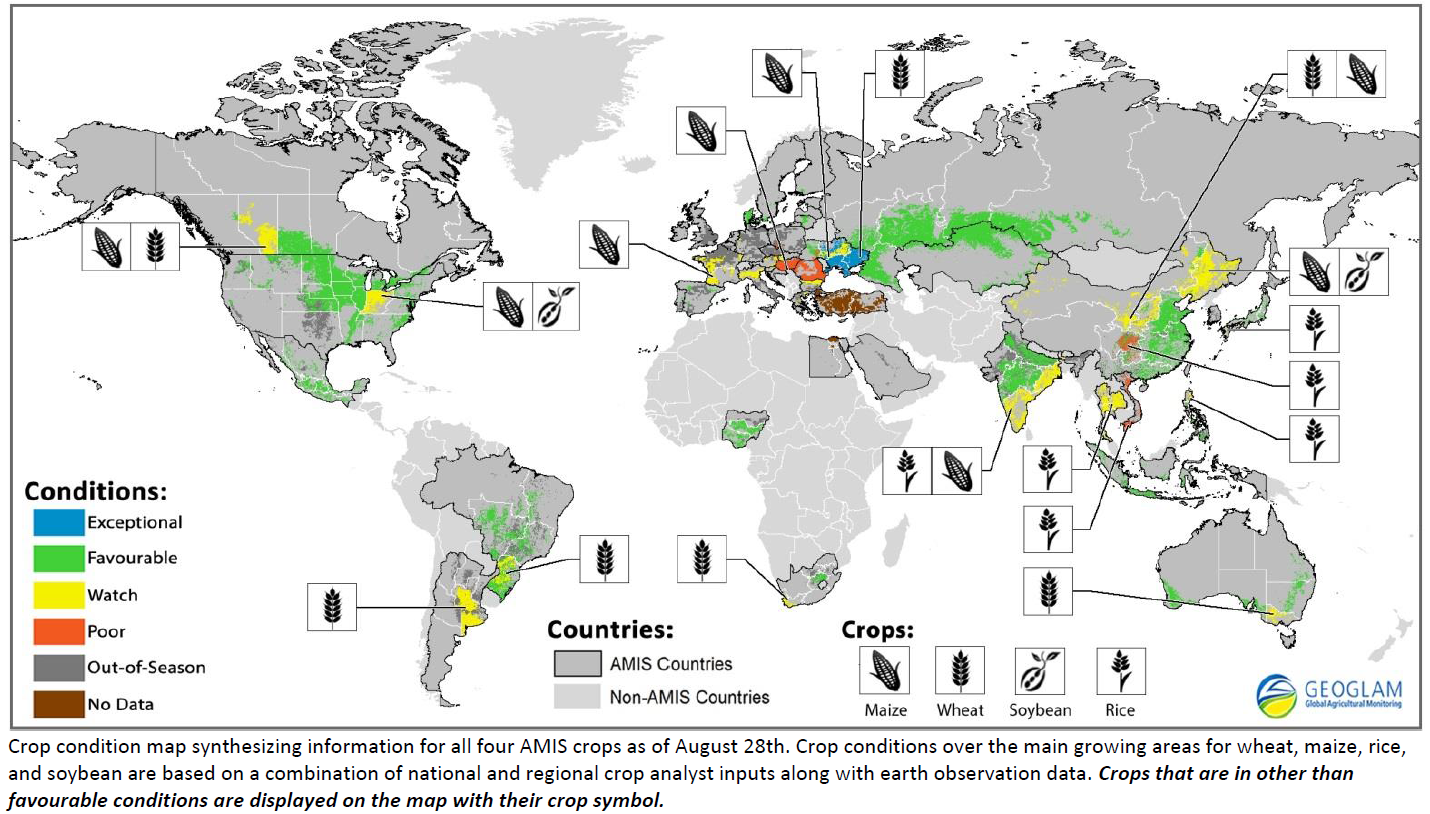

The AMIS Market Monitor highlighted El Niño's potential positive and negative effects on growing conditions for 2015/2016 depending on region, season, timing and strength. Indications are that the current El Niño could be one of the top four strongest since 1950. It is already impacting growing conditions in eastern and southern Asia, while its usual association in Australia with reduced precipitation in the east and warmer temperatures in the south have likely been moderated by increased sea surface temperatures across the Indian ocean. Its effects in southern Africa, South America, North America and Central Asia remain to be seen over the course of the winter and spring seasons.

In terms of policy developments, the first intervention purchases of grain from the 2015 crop began on 18 August in the Russian Federation. The Indian government implemented a 10 percent tariff on wheat imports 7 August to last until 31 March 2016, the first such measure in several years, and wheat farmers in Argentina adversely affected by floods will be benefiting from $4.3 million USD in tax breaks.

For details on additional policy developments, AMIS crop conditions and markets, and more:

AMIS Market Monitor no.31, September 2015

Files:

{kind=link}

{kind=link}

{kind=link}

{kind=link}