Global markets can help reduce climate-driven food insecurity

Climate change is almost certain to increase the volatility of agricultural output over the next 30 years—particularly in low-income countries in Africa south of the Sahara and other areas around the world where subsistence farming is a major source of food production. Climate-driven impacts such as droughts and extreme weather events will raise the risk of severe food shortages for smallholder farms and in rural and urban communities throughout those countries.

But production of staple commodities including maize, rice, wheat, and pulses is much less volatile at the global level than at the country or regional levels—and likely to continue that way even as temperatures rise. Thus, international trade and access to global markets have the potential to substantially reduce the risk of food insecurity, hunger, and malnutrition for low-income countries like Malawi and Bangladesh, helping to mitigate domestic food production volatility and to stabilize the prices paid by urban populations.

Recent projections for cereals, oilseeds and pulses based on the IFPRI IMPACT model (which also informs the FSP's Global Foresight Tool) highlight both the potentially substantial climate impacts on global production of staples and the potential importance of access to global markets as a means to reduce the risk of food insecurity in 2050.

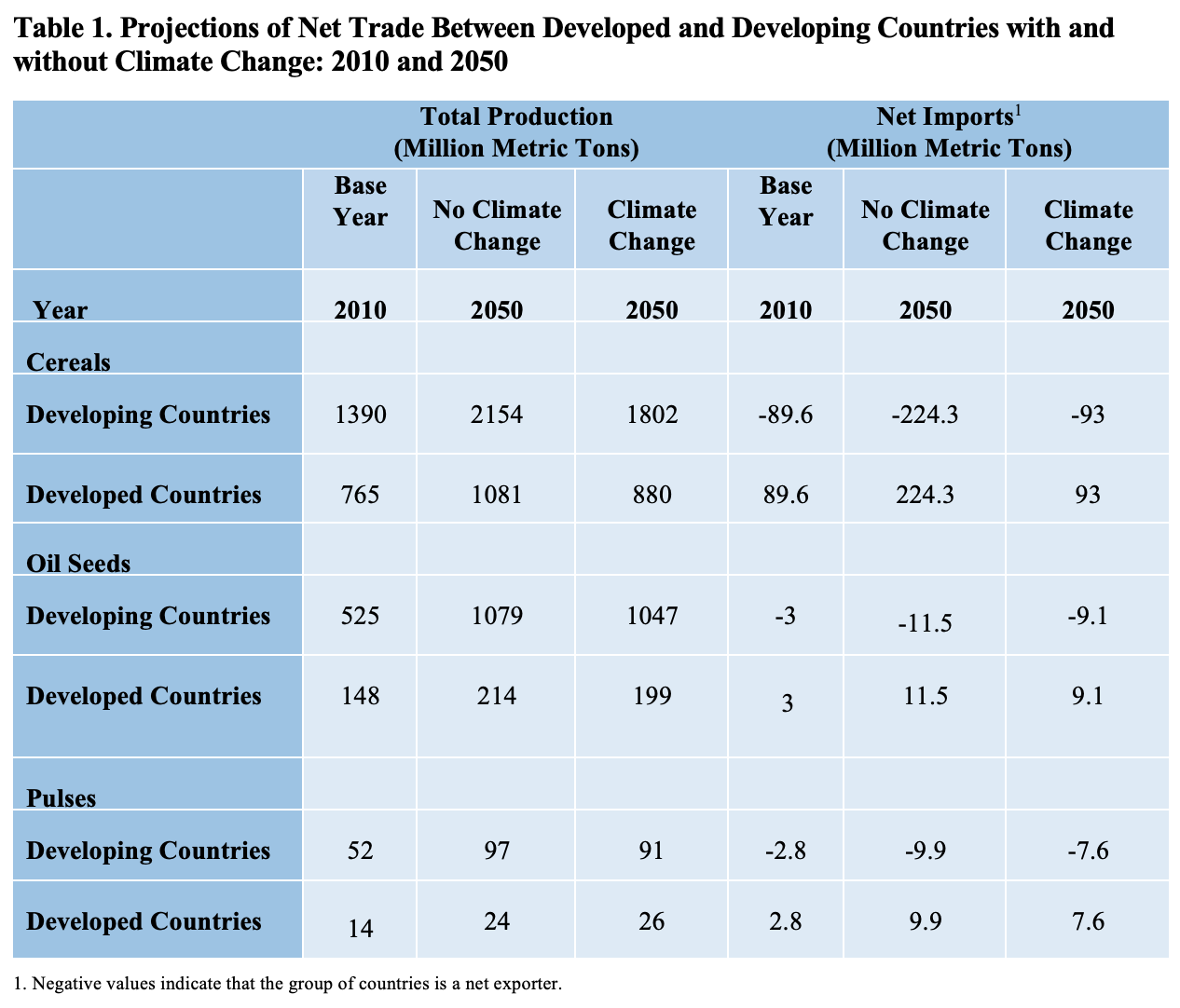

Table 1 shows that compared to 2010, global production of cereals, oil seeds, and pulses in 2050 will rise—but that climate change impacts will lead to much smaller increases in production of cereals in developing countries.

Meanwhile, oil seed and pulse production will almost double in developing countries, despite climate effects. One reason for this difference is that smallholder and larger farms in developing countries are likely to switch land away from maize production and towards those crops. In addition, developing country imports of all three categories of crops are projected to increase, rising by about 5% for cereals but tripling for oilseeds and pulses by 2050.

Given that trade in these staples—as well as for fruits and vegetables and other foods—is expected to increase, ensuring that developing countries have access to international markets, in which trade flows are not diverted by domestic policies or import or export constraints, will allow international exchange to help moderate climate-related food security risks.

The recent history of how governments in middle- and lower-income countries responded to the sharp increases in staple food prices between 2008 and 2012 is therefore a cause for concern. India, China, and other countries adopted restrictive trade policies (for example, export taxes or bans) to increase domestic food supplies, while driving up the prices other countries paid for critical food imports. To the extent that such trade-distorting policies remain in place, or are viewed as a viable response to price spikes, they have the potential to limit the food security benefits that accrue from more open trade as climate-driven production volatility grows.

Thus, maintaining and extending current World Trade Organization (WTO) trade and market access agreements—and specifically the WTO agreement on agriculture—can help to enhance long-term food security in the face of rising climate risks.

This post draws heavily on material included in a journal article by Vincent H. Smith and Joseph W. Glauber in Agricultural Economics titled "Trade, Policy and Food Security."

Vincent H. Smith is a Professor of Economics at Montana State University.